|

March

Newsline

|

|

March

Newsline

|

![]()

To read any article you are interested in; please click on the topic.

For the entire Newsline; please click on the heading.

Schools Must Report Hope Scholarship and Lifetime

Learning

Credit Info to IRS

The Internal Revenue Service has described information reporting requirements for 1998 that apply to certain eligible educational institutions with regard to the Hope Scholarship Credit and the Lifetime Learning Credit. These requirements are intended as interim requirements pending finalization by the U.S. Treasury Department.

Schools must submit IRS Form 1098-T, the Tuition Payments form for all students who are eligible to claim either the Hope Scholarship Credit or the Lifetime Learning Credit. The 1098-T must be submitted by March 1, 1999, for each student on whose behalf the school received payment or reimbursement for qualified tuition and related expenses for academic terms beginning in 1998. The name, address and taxpayer identification number of both the school and the student must be provided on the 1098-T. The form must also indicate whether the student was enrolled at least half time during any academic term beginning in 1998 and whether the student was enrolled in a graduate program. A single information report is being requested, even if more than one payment was received by the school during 1998.

Only tuition and fees count as "qualified tuition and related expenses." Amounts paid for courses involving sports, games or hobbies are not available for either credit unless part of the degree program. Charges for room and board, student activities, insurance, books, equipment, transportation, etc., do not count as "qualified tuition and related expenses."

Schools won’t be asked to provide the amount of qualified tuition and related expenses received for each student for 1998. They will, however, be asked for this information for 1999 and beyond.

All the information the school reports to the IRS on the 1098-T must also be reported to the student by Feb. 1, 1999. The school must also provide a telephone number that students may call if they have any questions on the reporting.

Schools making tuition refunds or reimbursements to students during 1998 which equal or exceed payments received on behalf of the student for tuition and expenses are not required to file Form 1098-T or furnish a statement to that student for 1998. Schools are also not required to file Form 1098-T for students whose tuition and expenses were waived or paid entirely with scholarships.

For purposes of providing these information reports, eligible educational institutions should provide reports on students who are enrolled in the institution for an academic term beginning in 1998. An institution should determine its enrollment for each term as taking place on any of the following three dates:

1. Thirty days after the first day of the academic term.

2. A date during the term on which enrollment data must be collected for purposes of the Integrated Postsecondary Education Data System administered by the Department of Education.

3. A date during the term on which the institution must report enrollment data to the state, its governing board or some other external governing body.

No penalties will be imposed on any school for failure to meet these requirements for academic periods beginning in 1998, provided that a good faith effort has been made to file information and furnish statements as required. A new form is in development to make it easier for schools to report student information. This form (Form W-95) will be available in time for reporting in 1999.

IRS Notice 97-73 contains detailed information on reporting requirements. Schools with questions should call the IRS at (202) 622-4910.

The Hope Scholarship Credit (see February 1998 Newsline) is available for qualified tuition and related expenses paid after Jan. 1, 1998, for academic periods beginning on or after Jan. 1, 1998. The Lifetime Learning Credit (see page 3) is available for tuition and expenses paid after July 1, 1998, for academic periods beginning after July 1, 1998. For a taxpayer to be eligible for either credit, qualified tuition and related expenses must be paid by the taxpayer to an eligible education institution for the taxpayer, the taxpayer’s spouse or any dependents. Payments by a taxpayer’s dependents are to be treated as having been made by the taxpayer. The Hope Scholarship Credit is available only to students enrolled at least half-time in the first two years of postsecondary education and can be claimed for no more than two years for each student.

LOSFA Says Farewell to Two Employees

Chole

Rackley resigned last month as the Office of Student Financial Assistance’s chief

legal counsel and head of the Legal and Policy Section. Chole, a graduate of LSU Law

School, began at LOSFA in September 1992. Besides her full plate of LOSFA duties she

also served as legal adviser to LOSFA’s governing commissions (LASFAC and LATTA) and

served on the Programs Regulations Committee of the National Council of Higher Education

Loan Programs. "It has been a great pleasure working at LOSFA all these

years," said Chole, who expressed her extreme pride in her staff and the work

they’ve accomplished. "I’m going to miss everybody." Chole

and her husband hope to start a family soon.

Chole

Rackley resigned last month as the Office of Student Financial Assistance’s chief

legal counsel and head of the Legal and Policy Section. Chole, a graduate of LSU Law

School, began at LOSFA in September 1992. Besides her full plate of LOSFA duties she

also served as legal adviser to LOSFA’s governing commissions (LASFAC and LATTA) and

served on the Programs Regulations Committee of the National Council of Higher Education

Loan Programs. "It has been a great pleasure working at LOSFA all these

years," said Chole, who expressed her extreme pride in her staff and the work

they’ve accomplished. "I’m going to miss everybody." Chole

and her husband hope to start a family soon.

LOSFA

staff members said good-bye to Winona Kahao Stone, who resigned from her position as head

of LOSFA’s Scholarship and Grant Division and is moving to Florida to be with her new

husband, Mike. Colleagues gathered Feb. 4 at Don’s Seafood to wish her the best.

LOSFA

staff members said good-bye to Winona Kahao Stone, who resigned from her position as head

of LOSFA’s Scholarship and Grant Division and is moving to Florida to be with her new

husband, Mike. Colleagues gathered Feb. 4 at Don’s Seafood to wish her the best.

Citibank (New York state) has signed a lender participation agreement with LOSFA. Citibank loans will be serviced by UNIPAC in Denver, Colo. The Citibank lender code number is 807743.

Also entered into LOSFA’s eligible lender list is FNB Chicago, Trustee for Educational Financial Group, lender #833471. They will be disbursed and serviced by USA Group.

Mary Genco is relinquishing her position as Assistant Director of Financial Aid at Louisiana State University for the position of Associate Director of Financial Aid at Southeastern Louisiana University.

Vivian Addison retired as financial aid counselor at Southeastern Louisiana University, where she has served for the last 24 years, to pursue other endeavors. Students, friends and colleagues gathered Feb. 20 in Hammond to wish her good-bye and good luck.

Best wishes to Joyce Brophy, Assistant Vice President and Student Loan Program Manager at Whitney Bank, who will be retiring March 21. Congratulations to Linna Alcoser, who will be taking over the reins from Joyce.

Mark Riley has replaced Chole V. Rackley as LOSFA’s new general counsel and head of the Legal/Policy Division. Mark has been an attorney and businessman for over 20 years with a master of laws in taxation. He served as President/CEO of an environmental company and has returned from a recent recall to active duty as a Colonel in the Marine Corps to support U.S. operations in Bosnia.

Gov. Foster has appointed William C. Jones to serve as Vocational Technical Representative for the Louisiana Student Financial Assistance Commission (LASFAC) and the Louisiana Tuition Trust Authority (LATTA). This appointment will fill the Commission/Authority’s final vacancy.

Roberts Beauty College, Covington, La., is under new ownership and is approved to participate in LOSFA’s loan programs. The school ID is #026009.

Baton Rouge Beauty College, school ID #012918, has announced that it has closed effective Feb. 26.

Moler Beauty College Inc. of Mandeville, La., also announced its closure effective Feb. 28. Its school ID number is 017106.

Some good news out of LOSFA’s Loan Operations Division: The Collections Section reports that in-house collections for state fiscal year 1997-98 through February is $5,284,398. That’s 113 percent of projection. Collections from all sources stand at $8,207,311, which is 95 percent of projection. The Pre-Claims Section received 19,731 Pre-Claims Assistance Requests for the first seven months of this state fiscal year and has been successful in averting 13,744 accounts from default. This represents a dollar amount of $65,524,550.

STARTing Line, the official newsletter of LOSFA’s START Saving Program, is available on the Internet at LOSFA’s website (www.osfa.state.la.us). Visit the site to see the latest news about the START Saving Program and its progress and information useful to present and future enrollees.

To receive a copy by mail,

write STARTing Line,

P.O. Box 91271,

Baton Rouge, LA 70821-9271;

or call Customer Services at (800) 259-5626, Ext. 1012.

Lifetime Learning Credit Available

Certain provisions of the Taxpayer Relief Act of 1997 will allow some taxpayers to be eligible to claim a nonrefundable Lifetime Learning Credit against their federal income taxes beginning July 1, 1998. The Lifetime Learning Credit may be claimed only for qualified tuition and related expenses for students in the taxpayer’s family enrolled in eligible educational institutions. A taxpayer’s family includes the taxpayer, the taxpayer’s spouse or eligible dependents, including children. The Lifetime Learning Credit is calculated on a per family basis, unlike the Hope Scholarship Credit which is calculated on a per student basis.

The credit is good for 20 percent of the taxpayer’s first $5,000 of out-of-pocket tuition and qualified expenses for all the students in the family until the end of 2002. After 2002, the credit amount will be equal to 20 percent of the taxpayer’s first $10,000 of out-of-pocket expenses. That means the maximum credit a taxpayer may claim is $1,000 through 2002 and $2,000 thereafter. These amounts are not indexed for inflation.

Taxpayers claiming a Hope Scholarship Credit for a particular student cannot apply the Lifetime Learning Credit toward that student’s expenses for that year.

The amount that can be claimed is gradually reduced for taxpayers with a modified adjusted gross income between $40,000 and $50,000 ($80,000 for married taxpayers filing jointly). Taxpayers with modified adjusted gross incomes above these amounts are not eligible to claim a Lifetime Learning Credit. The modified adjusted gross income limitation will be indexed for inflation in 2002 and thereafter.

The Lifetime Learning Credit may be claimed for payments of qualified tuition and related expenses made on or after July 1, 1998, for academic periods beginning on or after July 1, 1998. The first time taxpayers will be able to claim the deduction is when they file 1998 tax returns in 1999.

Only tuition and fees count as "qualified tuition and related expenses." Amounts paid for courses involving sports, games or hobbies are not available for the credit unless they are part of the degree program. Charges for room and board, student activities, insurance, books, equipment, transportation and similar expenses are not counted as "qualified tuition and related expenses."

Only the parent or the child, but not both, may claim the credit for the child’s expenses in a given year. If a person claims the child as a dependent on his or her federal income tax return, only that person may claim the Lifetime Learning Credit for the child’s qualified tuition and expenses. If no one claims the child on a federal income tax return, only the child may claim the credit for the child’s expenses. The child may not claim the credit on his or her income tax return if the child is claimed as a dependent on a parent’s return.

Students may take into account only out-of-pocket expenses when claiming the credit. Qualified tuition and related expenses paid with a Pell Grant or other tax-free scholarship, a tax-free distribution from an Education IRA or tax-free employer-provided educational assistance may not be used to calculate the credit amount. Tuition and expenses paid with a student’s earnings, a loan, a gift, an inheritance or personal savings are taken into account when calculating the credit amount.

Students taking only one course are eligible for the credit if the student isn’t claimed on someone else’s income taxes as a dependent. The credit is also available for those students taking courses at the graduate level.

Unlike the Hope Scholarship Credit, there is no limit to the number of years for which a Lifetime Learning Credit may be claimed for each student. Parents or students may claim the Lifetime Learning Credit for tuition and expenses made during the calendar year for an academic period that begins in January, February or March of the following taxable year. Because the credit doesn’t apply to expenses paid before July 1, 1998, it will not apply to tuition paid before that date to cover academic periods beginning before or after that date.

Instructions accompanying 1998 tax forms (for filing in 1999) will explain how to calculate the Lifetime Learning Credit and how to claim it on the tax return. If you have further questions on how the Lifetime Learning Credit affects you, contact your tax adviser. LOSFA, in summarizing these issues, is not rendering legal or tax opinions.

Before you know it, it will be Trailblazers time. We are urging high school guidance counselors to return nomination forms for the two Trailblazers Camps this summer. Forms and letters went out earlier this month. Counselors must return forms by April 15.

Trailblazers is a three-day camp which gives entering high school seniors an overview into some of the mysteries of college financial aid. Trailblazers are schooled in a number of topics, including state scholarships (TOPS), college admissions, financial aid processes, career choices, improving ACT scores, navigating the Internet for financial aid information and locating private scholarships. Armed with this information, students return to their schools able to assist their guidance counselors in helping fellow students to find financial aid.

LOSFA will host two Trailblazers camps this summer. The first camp, for students in the northern part of Louisiana, will be held on the campus of Northwestern State University in Natchitoches July 19-21. The second camp is for students in the southern portion of the state and will be held at Southeastern Louisiana University in Hammond, July 26-28. Room and board for each Trailblazers Camp will be provided by LOSFA. Transportation to and from each training site, however, is the student’s responsibility.

Trailblazers offer much to their fellow students and serve as a valuable asset to guidance counselors. To ensure their school’s participation, guidance counselors and/or principals must select a qualified junior and one alternate who are enthusiastic about the opportunity to be a Trailblazer. Nominees must be college-bound, effective public speakers and, most importantly, leaders among their peers. The student with the highest g.p.a. is not necessarily the best choice for a Trailblazer or alternate. The best Trailblazer is the one who can motivate his or her classmates and help them prepare for their future life at college.

For more information on

Trailblazers

please call LOSFA’s Customer Services Division

at (800) 259-5626, Ext. 1012.

An Invitation to 1997 Trailblazers

Hey, 1997 Trailblazer, we want to hear from you.

The Louisiana Office of Student Financial Assistance wants Trailblazers to tell what they did last year to prepare their fellow classmates for college. What did you do to "blaze the trail"?

Did you lead workshops? Cover bulletin boards with flyers and brochures? Offer tours of the Internet?

The Trailblazer with the most creative way of reaching fellow students will be invited to give a presentation at one or both of the upcoming Trailblazer camps this July in Natchitoches or Hammond. The presentation is intended to give future Trailblazers advice on how to reach their classmates with important information about their futures.

Trailblazers, just submit a one-page summary of your trail-blazing activities during the past year. Tell us what you’ve done. Write to:

Jennifer Burton

Louisiana Office of Student Financial Assistance

P.O. Box 91202, Baton Rouge, La. 70821-9202

or fax information to (225) 922-0790

or e-mail to jburton@osfa.state.la.us.

The Common Manual Policy Committee has reviewed industry comments on proposals that recommend operational efficiencies and enhancement to the Pre-Claim Request Form and expect it to be approved this month.

The second phase of the Common Claim Initiative (CCI) was completed when the common Pre-Claim and Claim form was approved in February. New Pre-Claim and Claim requirements will phase in through March 1, 2000, when certain elements of claim review will be transferred to Program Review.

Two proposals distributed for comment have been deferred by the Policy Committee for further development: proposal #203 Ineligible Borrower Claims and proposal #199 Comaker and Endorser Due Diligence Schedules and Activities. In proposal #203, the penalty for submission of a claim on which the final demand has not been sent timely has been corrected to conform to the consensus reached by the industry representatives responsible for the development of the standardized Claim Form. Proposal #199 has been clarified regarding the lender’s resubmission deadline when a claim has been returned for lack of endorser due diligence. In addition, a new proposal has been drafted to introduce an integral facet of the process associated with the standardized claim form, three lender claim review status categories. These three proposals will be redistributed for a second comment period.

Policy proposals relating to the third phase of the CCI project, Skip Tracing, will also be distributed for comment. The objective of these proposals is to align the guarantor requirements for the monitoring of skip tracing activities.

All policy proposals relating to the Preclaim Request Form, the standardized Claim Form and Skip Tracing are on a schedule to be included in the July 1998 Common Manual update.

The Emergency Student Loan Consolidation Act (ESLCA) signed into law by President Clinton on Nov. 13, 1997, became effective upon enactment. Preliminary policy proposals have been drafted to align the Common Manual with the terms of the Act. These proposals should be released for industry comment and approval in time for inclusion in the July 1998 Common Manual Update.

Education Department Requires

Year 2000 Compliance

Postsecondary educational institutions which participate in Title IV Student Financial Assistance (SFA) Programs must achieve Year 2000 compliance by Jan. 1, 1999, according to the U.S. Department of Education. Computer systems must be able to store, process and report date data in ways that differentiate between years prior to 2000 and the year 2000 and beyond.

ED defines Year 2000 Compliant as applications that "are capable of correct identification, manipulation and calculation using dates, including leap years, outside of the 1900-1999 year range and have been tested as such." Few systems currently in use were designed with the ability to process dates later than 1999.

The issue is critical because many computer systems were not designed to accommodate a four-digit year. In many cases data is stored and processed using only the final two digits of the year, which could result in serious processing errors and disruptions to student aid delivery and accountability. ED strongly encourages institutions to develop an aggressive strategy and action plan for addressing this issue.

Some ED data such as current record descriptions in the EDExpress software (including the Direct Loan modules), the National Student Loan Data System (NSLDS) and Student Status Confirmation Report (SSCR) processing already require four digits for the year. Other systems, including Pell Grant Payment Reporting, Fiscal Operations Report and Application to Participate (FISAP) and Education Central Automated Processing Systems (EDCAPS) will soon require the four-digit year.

Some data already being transmitted to ED from students and institutions contain dates that go beyond 2000. The Free Application for Federal Student Aid (FAFSA) asks applicants for the date they expect to complete their academic program. SFA loan applications require the submission of the borrower’s anticipated graduation or completion date. Program completion dates are also required to be sent from institutions to the NSLDS in the SSCR and other enrollment tracing processes.

Systems other than just financial aid systems must be fully Year 2000 compliant, such as systems which deal with registration, admissions, student accounts and financial transactions. Vendor-supplied software or the services of a third party for any portion of SFA processing must become Year 2000 compliant by the Jan. 1, 1999, deadline. The fact that a third party (vendor or servicer) made an error does not relieve an institution of its responsibility for compliance with all laws, regulations and policies relating to the Title IV SFA programs.

During the assessment phase of determining compliance with Year 2000, institutions need to assess the following data systems that either provide data to or receive data from postsecondary educational institutions that participate in Title IV Student Financial Assistance Programs:

• Multiple Data Entry (MDE), responsible for inputting application data provided by applicants for Title IV student financial assistance;

• Central Processing System (CPS) which processes applicant data including editing, database matches and the calculation of an expected family contribution and then sends results to applicant and institution(s);

• Recipient Financial Management System (RFMS) which accepts and processes Pell Grant payment data from institutions and then returns results to institutions and transmits summary data to ED’s financial systems;

• Campus Based System (CBS) which collects FISAP data, processes edit reports, makes tentative and final awards and reports to ED’s financial systems;

• Direct Loan Origination (Center) System (LOC) which accepts Direct Loan origination records, prom note data and disbursement data from institutions, edits data, returns acknowledgments and submits data to Direct Loan Servicing;

• Direct Loan Service System which accepts Direct Loan origination and disbursement data from LOC, services (billing, collecting, customer service) loans and provides data to NSLDS, ED’s fiscal systems, etc.;

• National Student Loan Data System (NSLDS) which accepts data from lenders, guaranty agencies, institutions and other ED systems, interfaces with CPS for student eligibility determinations, calculates default rates and provides data to other ED systems;

• Postsecondary Education Participants System (PEPS) which maintains data on all participants in ED’s student aid system, including institutions, lenders and guaranty agencies.

This list does not include other ED systems such as EDCAPS and those used for statistical purposes, including the Integrated Postsecondary Education Data System (IPEDS), although these systems must also be Year 2000 compliant. Also, institutions must make certain that other interfaces they utilize in the administration of Title IV aid, such as those with Federal Family Education Loan (FFEL) lenders and guaranty agencies, are also Year 2000 compliant.

The complexity of the problem of Year 2000 Compliance is demonstrated by the potential awkwardness of a system that stores date information using only the last two digits of the year, the number of internal calculations and processes that an institution’s data systems may contain that might not account for the change to Year 2000 and beyond, the possiblility of data corruption which might take place when an error, even on a short-term basis invisible to the owner of the system, resonates throughout the system and perhaps spills over to others and disruption of a data system resulting in missed filing deadlines or delays in the processing or disbursement of student aid.

ED urges financial aid offices to contact the Chief Information Officer or information technology personnel of their institution to request information regarding the Year 2000 compliance plan and progress to date. It also urges FAOs to seek Year 2000 information from any third party vendors or servicers that provide them with software or other SFA services. FAOs are reminded to make certain that the plan includes the proper procedures and time frames for insuring that their institution will be able to meet the deadline. Additional information will be available on ED’s upcoming "Year 2000 Compliance Information and Best Practices" website. Questions regarding the year 2000 compliance requirement may be e-mailed to ED’s Program Systems Service staff at ope_y2k@ed.gov.

"Affording

College"

Airs Statewide on LPB Network

"Affording College," a one-hour live program addressing all areas of postsecondary education financing, aired statewide on the Louisiana Public Broadcasting (LPB) network on Sunday, Feb. 22. The program was sponsored by the Louisiana Public Facilities Authority (LPFA), Louisiana Office of Student Financial Assistance (LOSFA), Louisiana Association of Student Financial Aid Administrators (LASFAA) and the Louisiana Board of Regents.

The broadcast dealt with various

types of scholarships, work/study programs, eligibility for loans and other federal

programs, the financial aid application process, the awards process and costs of

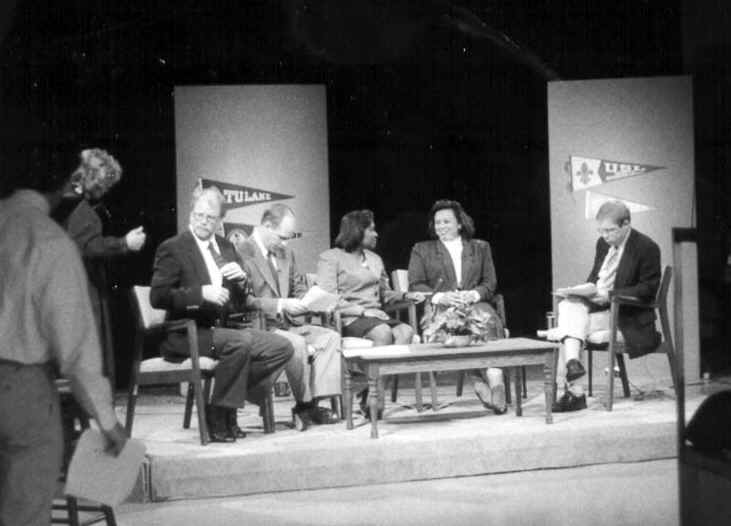

education. Serving as panelists were (top photo, left to right) Melanie Amrhein (LSU-Baton

Rouge), Frank Candalisa (Our Lady of Holy Cross College) and Gracie Guillory (LSU-Eunice).

Pictured with the group is LPB program moderator Barry Irwin.

The broadcast dealt with various

types of scholarships, work/study programs, eligibility for loans and other federal

programs, the financial aid application process, the awards process and costs of

education. Serving as panelists were (top photo, left to right) Melanie Amrhein (LSU-Baton

Rouge), Frank Candalisa (Our Lady of Holy Cross College) and Gracie Guillory (LSU-Eunice).

Pictured with the group is LPB program moderator Barry Irwin.

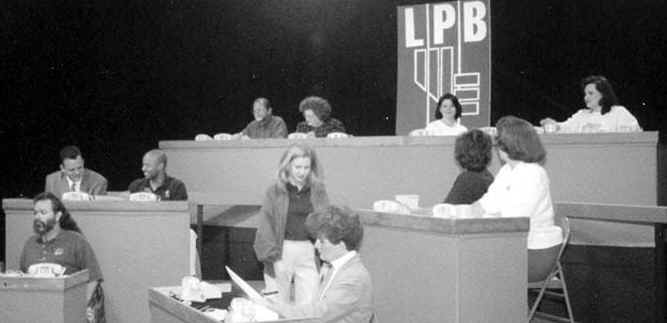

Panelists for the second half of the

telecast (above photo, left to right) included Dr. Jimmy Clark (Louisiana Board of

Regents), Chuck Perrodin (LPFA), Pamela Malveaux (LOSFA), Ms. Guillory and Mr. Irvin.

Panelists for the second half of the

telecast (above photo, left to right) included Dr. Jimmy Clark (Louisiana Board of

Regents), Chuck Perrodin (LPFA), Pamela Malveaux (LOSFA), Ms. Guillory and Mr. Irvin.

The program also allowed viewers to call in questions which were answered on the air by panelists or by telephone volunteers from the financial aid community. Shown in the bottom photograph are telephone volunteers (bottom row, left to right) Terry Martin (LSU), Johanna Miller (LPFA), Diane Pfeifer (LOSFA), (middle row, left to right) Dale Hilton (LOSFA), David Thomas III (LPFA), Joanie Leggio (LPFA), Jennifer Burton (LOSFA), (top row, left to right) Gus Wales (LOSFA), Michelle Klafke (LOSFA), Kim Tanner (LSU) and Judith Vidrine (LSU).

More than 100 viewer calls on a wide variety of financial aid related subjects were answered during the broadcast.

Click here ![]() to return to March Newsline Topics

to return to March Newsline Topics

Click here ![]() to return

to Newsline Home page

to return

to Newsline Home page